What is the Medicare Levy?

The Medicare Levy is a payment you make to the government every year at tax time. This money is used by the government to fund the public health system – public hospitals, urgent care clinics etc

This payment is generally approximately 2% of your income where you may get a reduction or exemption depending on you or your spouses income and circumstances. This payment is generally withheld by your employer from your salary and wages.

Who is exempt from this payment?

- There are the minority of income earners who may be exempt or are eligible for a reduction in their Medicare Levy such as:

- Low income earners (less than $27,222)

- Family taxable income less than $45,907

- Blind Pensioner

- Entitled to full free medical treatment under Defence

- Force arragements or Veteran Affairs Gold Card

- Foreign residency

- Not entitled to medicare benefits

Case Example #1 – Medicare Levy

Kristine earns a taxable income of $75,000 – she is single, has no dependents and is not eligible for any medicare levy exemptions.

Kristine pays 2% of her total taxable income = $75,000 x 2% = $1500

Case Example #2 – Medicare Levy

Steven earns $25,000. He is single, has no dependents and is not eligible for any Medicare levy exemptions.

Steven pays no Medicare Levy as his income is considered a low income earner and is below the Medicare Levy threshold.

What is the Medicare Levy Surcharge (MLS)?

The Medicare Levy Surcharge (MLS) is a separate payment made to the government during tax time. It is purely based on level of income of a single or a family and varies from 0-1.5%. The important thing to note is that this is in addition to the Medicare Levy.

Now you might be thinking… I could potentially be paying a total of 3.5% extra tax to the government? The answer is yes but kind of. I don’t even use the public health system?1!?! Why the hell do I have to pay $3.50 for every $100 I earn?!?!

Let’s first talk about how it is calculated – as above, it’s purely on income thresholds.

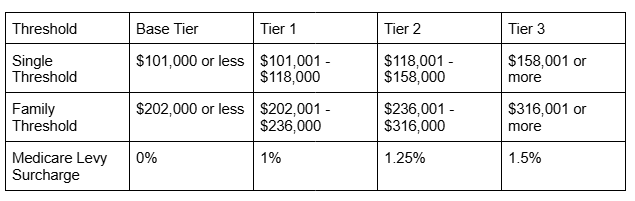

How much is this surcharge?

The MLS Income thresholds and rates for 2025-2026 is summarised in the table below:

How can I avoid paying for the Medicare Levy Surcharge?

You can dodge the Medicare Levy Surcharge if you, your spouse and your dependent children have an appropriate level of private patient hospital cover – this is normally any hospital cover you can get with a private insurer.

If you hold private health insurance for only a portion of the time during the tax year – this will be apportioned appropriately.

Case Example – Medicare Levy Surcharge

Kristine gets a promotion at her job and her taxable income increases to $115,000 per year.

Scenario #1

If she has no private health insurance hospital coverage – since she falls into Tier 1 category – she will pay 1% Medicare Levy Surcharge.

1% x $115,000 = $1150

Scenario 2

If she has private health insurance cover for 100 days of the 365 days in the 2025 Financial year – she will have to pay for the 265 days she does not hold an appropriate cover.

265/365 x 1% x $115,000= $834.93

Scenario 3

If she gets private health insurance for the full financial year – she will be charged no Medicare Levy Surcharge

Summary

The Medicare Levy is approx 2% of your taxable income for most income earners.

The Medicare Levy Surcharge is an extra tax payment made if you (or your spouses) income is over a certain threshold – this is in addition to the Medicare Levy (on top of)

Understanding why the MLS exists, how it affects you based on your income and what you can do to avoid paying more than you need is a prudent way of managing your costs as your income increases. Remember an extra dollar paid to tax is a dollar less you can save!